Yext 2026 Consumer Search Behaviors Report

Yext 2026 Consumer Search Behaviors Report

Ask, Verify, Act – How Consumers Navigate Local Search in the Age of AI. What 3,848 people worldwide told us about how they find, evaluate, and choose local businesses in 2026.

Introduction

The AI search tipping point has already happened

By now, marketers know that their brand should be visible in AI search.

“AI search” and “AI agents” have dominated headlines for months. But often, it still feels like the industry is admiring the problem of a changing search landscape rather than taking concrete steps to meet customers where they make decisions today.

With this challenge in mind, Yext surveyed 3,848 consumers globally about their local search habits: which tools they really use, how much they trust the results, and what ultimately drives them to act. What the data reveals is a picture more complex than most prevailing narratives around AI search would suggest.

Three themes run through the findings. First, AI adoption is broad, growing, and no longer confined to any one demographic or category. Second, consumer trust in AI is real – but it has not replaced the need to verify, and the channels people turn to for verification are the same ones that have always driven purchase decisions. And finally, the buyer journey is not a neat sequence of steps but a fluid, multi-surface process in which AI, reviews, social, and traditional search all play distinct and complementary roles.

Below, we’ll dive into the full data set from the global survey.

Consumer search has changed

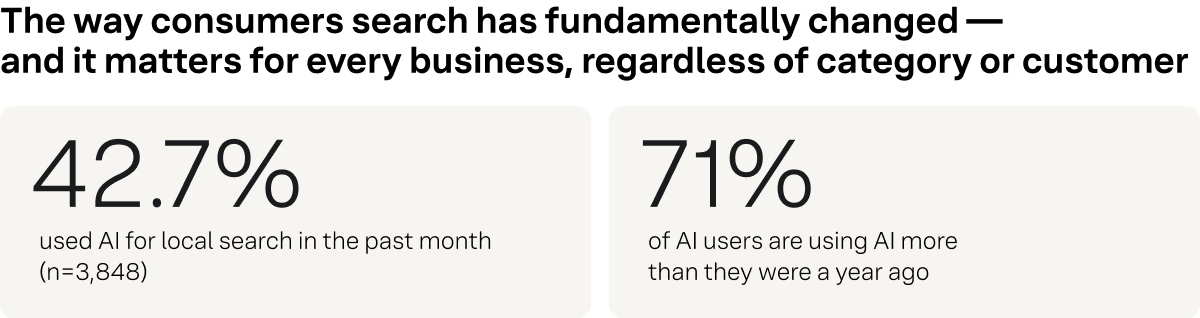

The first thing the data makes clear is that AI-driven local search is no longer an early-adopter behavior. It has entered the mainstream: nearly half of all global respondents – 42.7% – used an AI tool for local search in the past month.

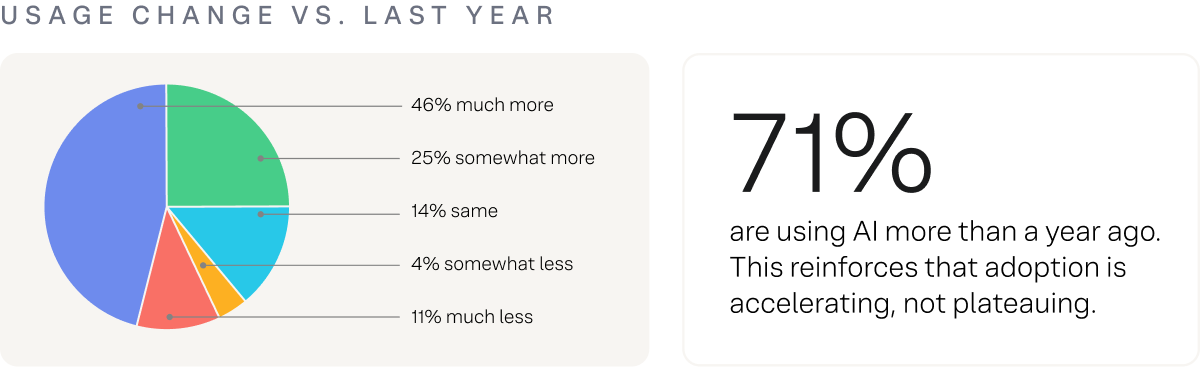

That figure alone is striking, but what makes it more significant is the adoption trajectory behind it: 71% of those AI users say they are using AI more than they were a year ago. Broken down further, 46% say they are using it “much more” and 25% say “somewhat more.” This is not a trend that is peaking; it’s still accelerating.

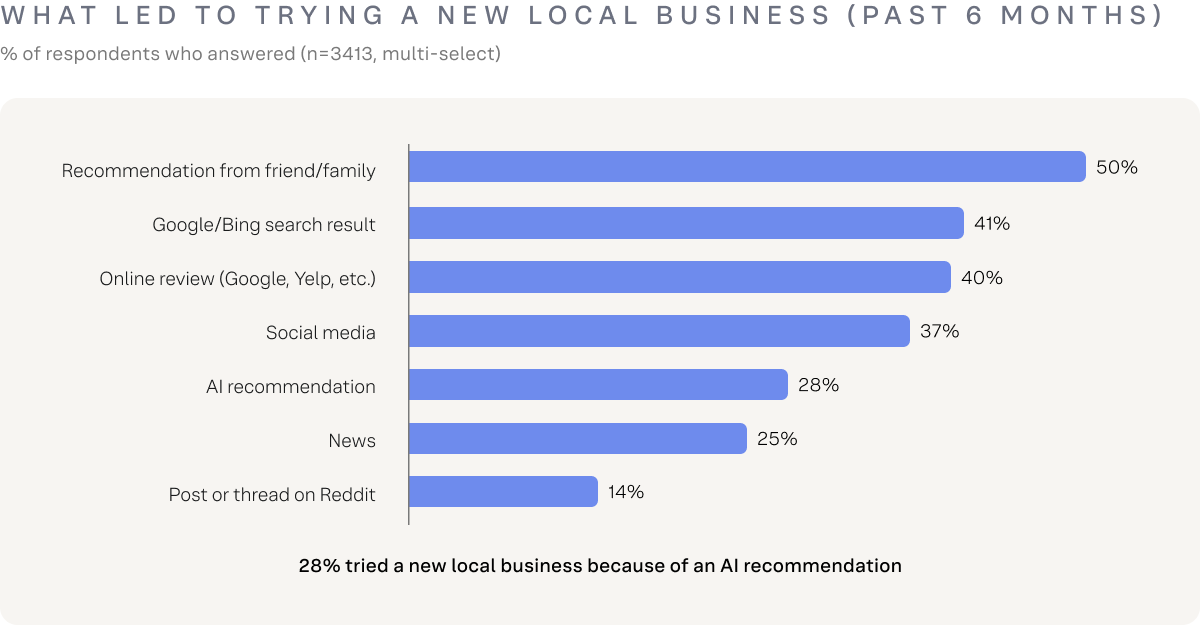

And the practical impact is already showing up in where new customers come from. In the past six months, 28% of respondents tried a new local business specifically because of an AI recommendation. That’s a meaningful share of new customer acquisition now flowing through an AI channel – and one that most brands are not yet optimized for.

On demographics: the highest-value consumers are moving fastest

North American data from this research cycle reveals a particularly important signal for marketers targeting high-income segments.

At $150k+ household income, AI has already overtaken Google as the starting point for local search – 54.5% start their journey with AI.

In other words: the consumers with the most purchasing power are already beyond the tipping point.

| At $150k household income: 54.5% start their search with AI. Among the highest-income consumer segments, AI has already surpassed Google as the primary starting point for local search. Full North American demographic data is available here. |

|---|

But despite this fast-moving cohort of high-income customers, the shift to AI is notably broad. Meaning: it is not concentrated in one category or only one type of shopper.

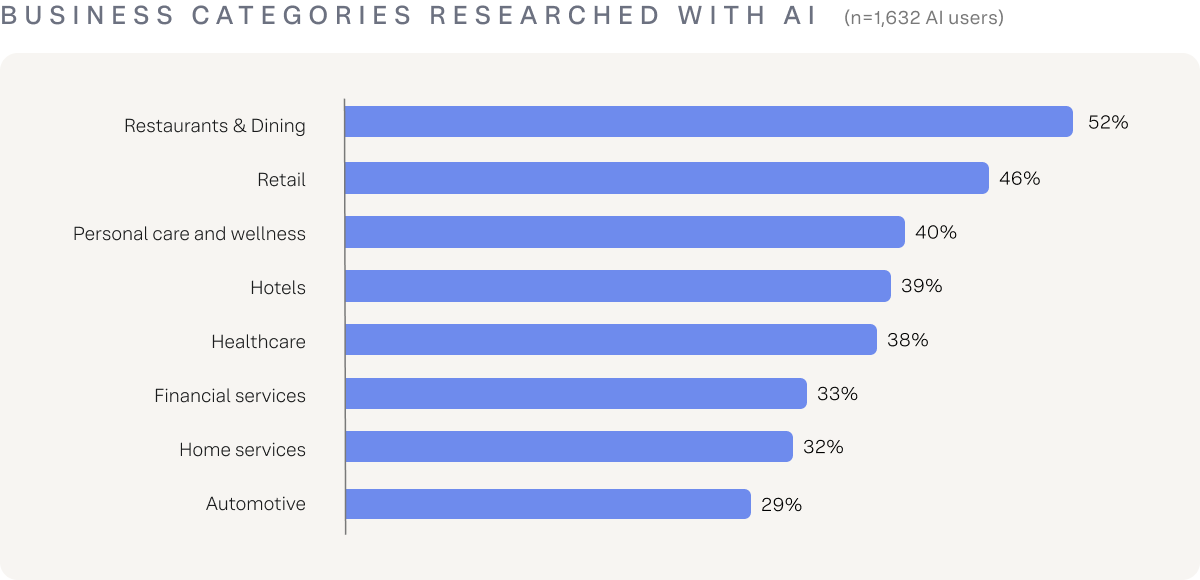

Business categories researched with AI span the full spectrum – from restaurants and dining at the top to automotive at the bottom – with the distribution between them relatively flat. This pattern confirms that no category of brand or business gets to treat AI visibility as someone else’s problem.

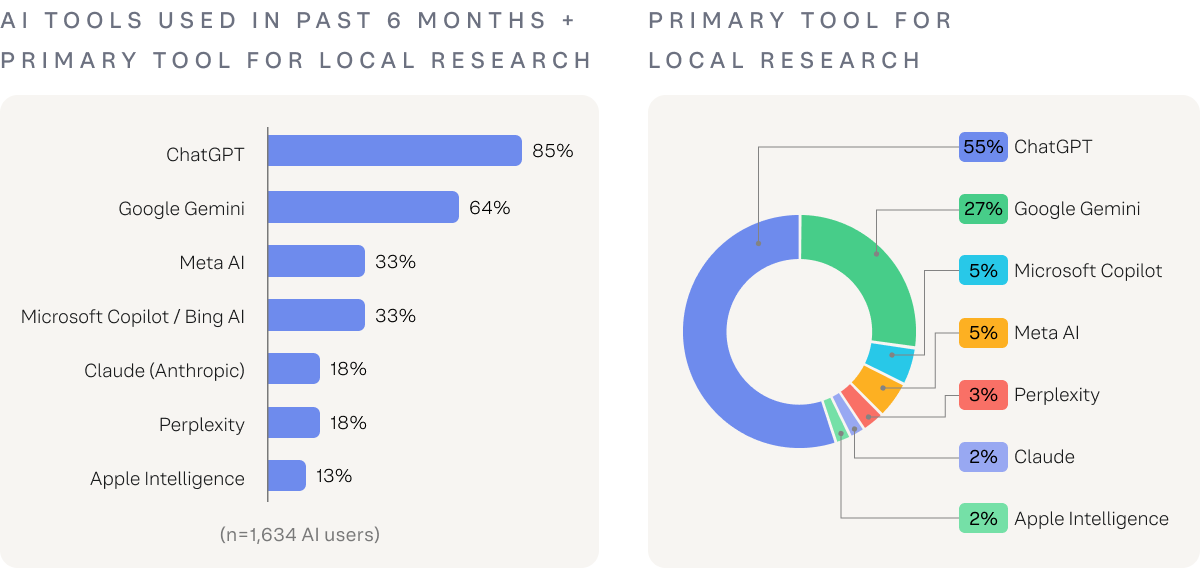

The competitive AI landscape adds even more complexity. ChatGPT leads tool usage among AI users, followed by Google Gemini, Meta AI, and Microsoft Copilot. So, brands can’t necessarily optimize for a single AI surface. They are potentially visible – or invisible – across multiple platforms simultaneously.

The growth pipeline

Finally, looking at the small percentage of AI non-adopters, the pipeline for future growth is clear. Among current non-adopters, 47% say they are somewhat or very likely to try AI for local search in the next six months.

The current 42.7% global adoption rate is a floor, not a ceiling. The next wave of AI searchers is already forming – and the data shows that most of their barriers are about habit, not trust.

Reviews and social signals

High AI adoption and growing consumer trust in AI are real. But they don’t tell the full story – and that’s where most brands are leaving money on the table.

High AI adoption and growing consumer trust in AI are real. But they don’t tell the full story – and that’s where most brands are leaving money on the table.

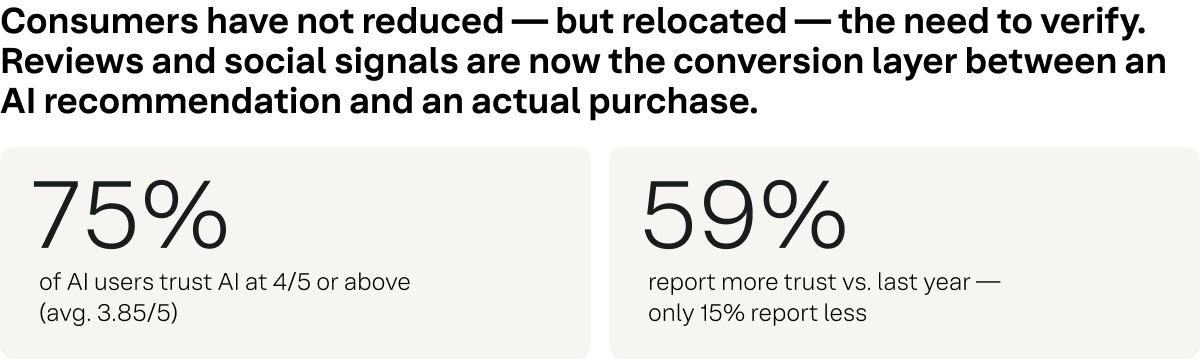

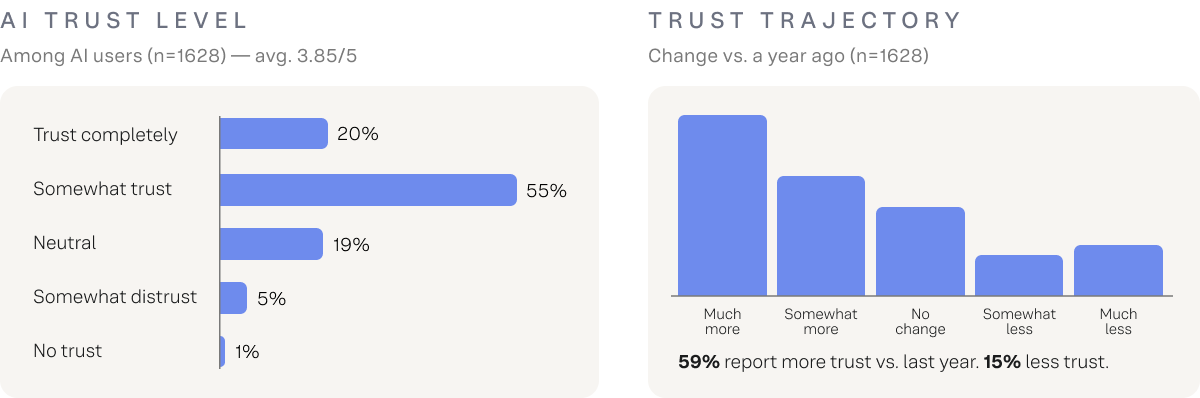

Among AI users globally, 75% rate their trust in AI local business recommendations at 4 or 5 out of 5, with an average score of 3.85 out of 5. And 59% report that their trust has grown over the past year, compared to just 15% who say it has declined. By any reasonable measure, AI recommendations have earned genuine consumer confidence.

And yet, nearly every AI user still verifies before acting.

The verification loop

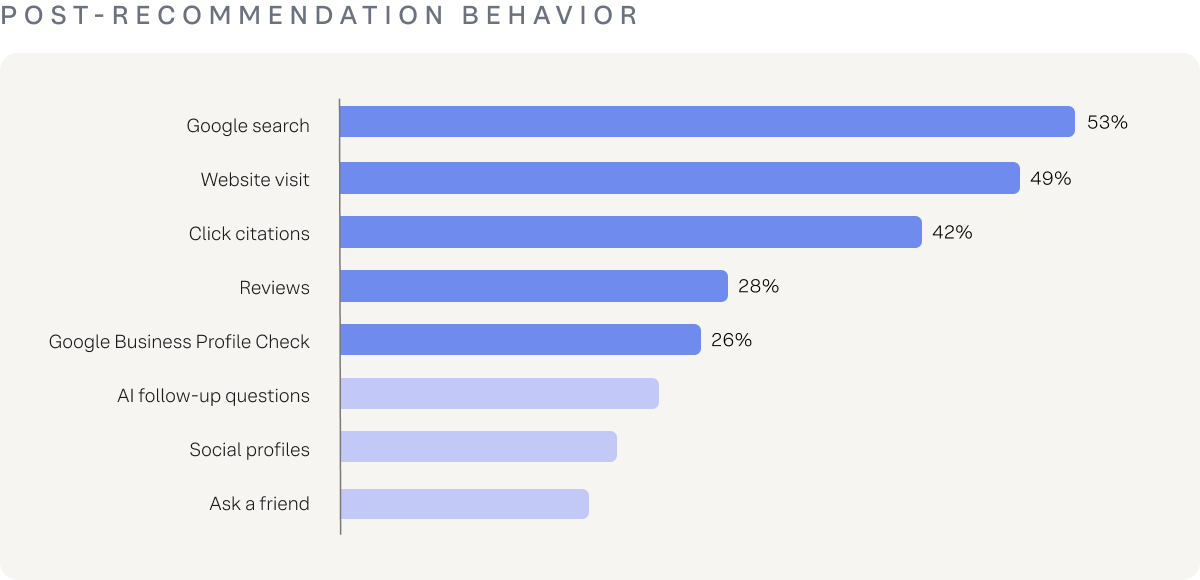

If there’s one standout finding from the survey, it might be this: no matter how much users say they trust AI, only 5% move directly from AI answer to purchase.

So, what do they do instead?

They take a series of verification steps.

After receiving an AI recommendation, more than half – 53% – search Google or Bing to verify or learn more. Nearly as many (49%) visit the business’s website directly. A significant share (42%) click through to the sources or citations the AI provided. Then 28% look for reviews on Google, Yelp, or similar platforms, and 20% check the business’s social media profiles.

Again, these verification rates hold nearly constant regardless of how much a consumer trusts AI. Checking up on a recommendation is simply how modern purchase decisions get made. What has changed is where verification happens – and that shift has direct implications for which channels brands need to maintain with care.

| After an AI recommendation: 53% search Google, 49% visit the website, 42% click AI citations, 28% check reviews, 20% check social. Every top post-recommendation action is a verification step. The channels brands rely on for conversion are the same ones consumers turn to after an AI rec. |

|---|

What drives the purchase decision

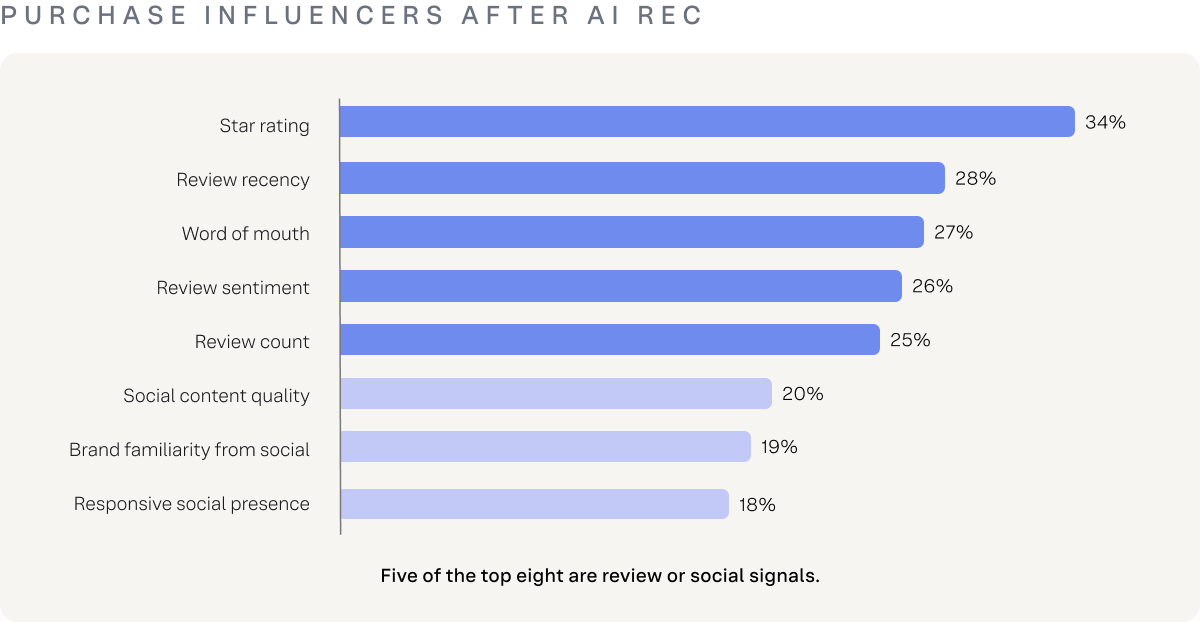

When asked what influences their decision to make a purchase after receiving an AI recommendation, consumers tend to rank review signals above everything else.

Star ratings on third-party review platforms rank first. Review recency ranks second. Review content and sentiment rank fourth. Total review count ranks fifth. Word of mouth from a trusted contact ranks third – which is itself a form of peer validation. Social media content quality and brand familiarity from social round out the top eight.

Given this, it’s a major brand mistake to treat reviews as “just” a reputation management function. In reality, reviews are the conversion layer between an AI recommendation and an actual customer. A brand optimized for AI visibility but not for review quality will generate recommendations that do not convert.

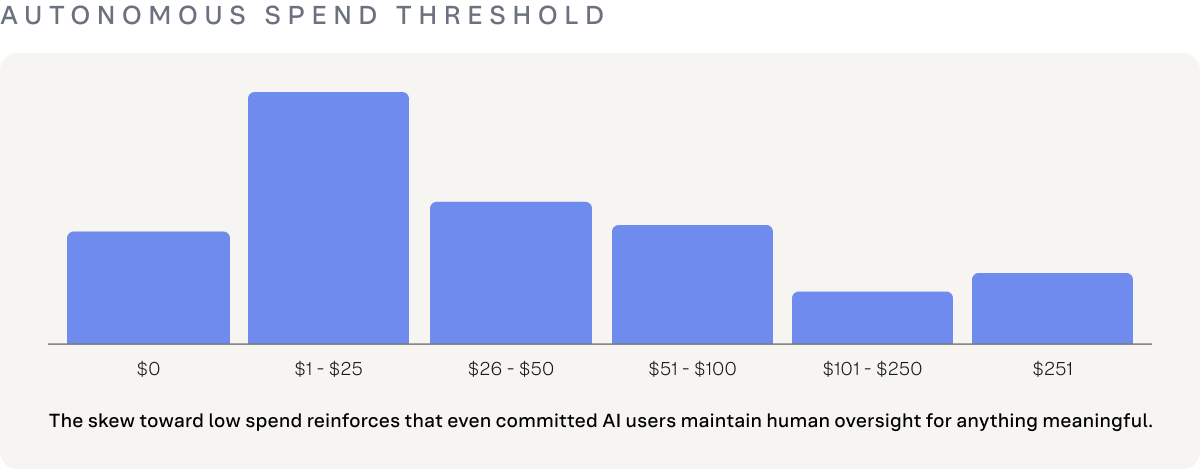

The autonomous spend threshold

One additional data point puts the verification behavior in useful context. The median amount consumers globally are comfortable letting AI spend on their behalf without additional review is just $25. Even among consumers who say they are comfortable with AI-assisted transactions, the threshold for fully unsupervised action is low. For any purchase above that level – which describes most commercially significant decisions – human verification is built into the process.

The takeaway? AI visibility alone isn’t enough. Brands who aren’t present across every channel someone might consult as part of their verification process may show up for customers, but they won’t convert them.

The verification loop

The journey isn’t as simple as “AI for research, traditional platforms for purchase.” People are using AI for everything – and the verification loop runs at every stage.

The picture that emerges from the first two findings might suggest a clean division of labor: AI for discovery, traditional platforms for decision.

But the data doesn’t support that framing. The reality is considerably more fluid – and more challenging for brands to manage.

AI spans the entire buyer journey

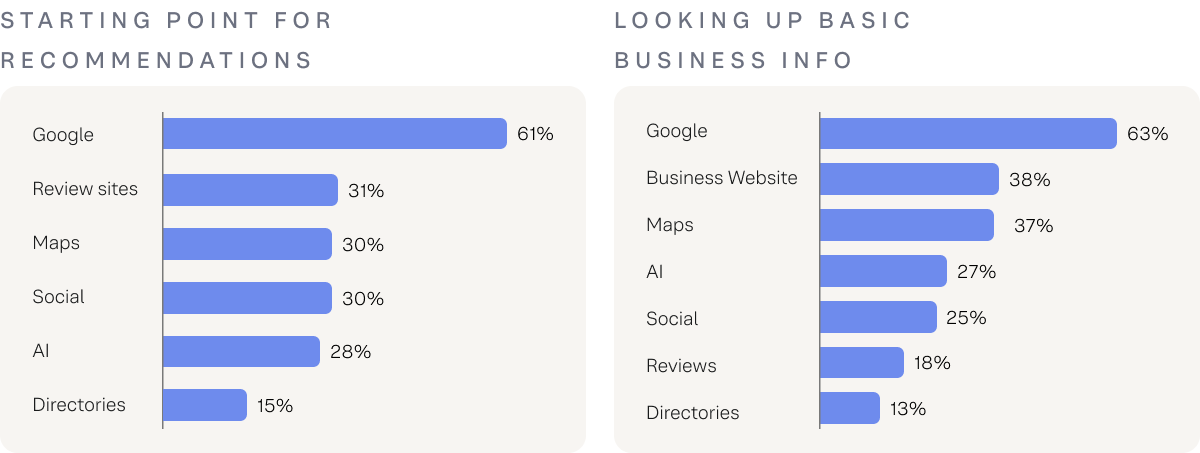

AI is embedded throughout the buyer journey, not just at the top. When consumers look up basic business information – hours, location, contact details – AI ranks as just the fourth most common tool used, behind Google, business websites, and maps apps. This is not a discovery platform sitting at the front of the funnel. It is a research layer people return to at multiple points.

When starting a recommendation search specifically, AI ranks fifth, behind Google, review sites, maps apps, and social media. This is the right framing: AI is one node in a multi-channel journey.

And across all use cases – from thorough pre-decision research to quick recommendations – the distribution is notably flat. There is no single dominant use case. Consumers are using AI as a research analyst, a comparison tool, a shortlist generator, and a quick-answer engine, often in the same session.

| All AI use cases score within a narrow range – thorough pre-decision research ranks #1, quick recommendations #2. There is no single ‘right moment’ to be visible in AI search. Brands must be citable at every stage of the buyer journey. |

|---|

Social media spans the full funnel

Social media plays an equally significant and often underestimated role throughout the journey. Globally, social media is the second most popular tool for local search overall (behind traditional search engines) and the fourth most common starting point for recommendation searches. After receiving an AI recommendation, 20% of consumers check a brand’s social media profiles as a verification step.

Social is present at both ends: it is where a large share of consumers begin, and it is part of the scrutiny a brand faces when a consumer decides whether to trust what AI told them. Even if it’s challenging for brands to track, social media’s role in both active and passive discovery through the full funnel can’t be overstated.

Reviews from discovery through decision

Reviews follow a similar cross-journey pattern. Review sites rank second as a starting point for recommendation searches – ahead of maps apps and social media. And as noted in the previous section, review signals (star rating, recency, sentiment, volume) dominate the list of purchase influencers after an AI recommendation. Reviews are not the last step. They show up at the beginning of the journey, too.

The final takeaway? The job isn't to optimize for one AI touchpoint. It's to be the brand AI can confidently cite at any of them – and at any time in the purchase journey.

What this means for brands

The picture that emerges from this data is not simple – and that’s exactly the point.

The brands that win in this landscape will not be the ones that chase a single channel or bet everything on one type of visibility. They will be the ones that understand how the pieces fit together: AI has changed where the journey starts and how it unfolds, but it has not changed the fundamental truth that trust is built across every touchpoint someone encounters – before, during, and after a recommendation.

That means three things need to be true at once.

- Brands need to be in the AI answer set — which requires accurate, structured, machine-readable data that AI engines can confidently retrieve and cite.

- Brands need to hold up under scrutiny — because the vast majority of consumers will verify what AI tells them through reviews, Google, and social, and what they find there determines whether a recommendation becomes a customer.

- Brands need to show up consistently across every surface consumers use to research, compare, and decide — because the buyer journey is no longer linear, and the moment of influence can happen anywhere.

None of these is a replacement for the others. AI visibility without a strong verification layer generates recommendations that don’t convert. A strong review presence without AI visibility means missing the moment entirely for a growing share of the market. And social media, often treated as a separate discipline, turns out to be both a discovery channel and a conversion driver — one whose influence shows up most clearly at the exact moment a consumer decides whether to act on what AI told them.

The brands that get all of this right share one thing in common: they don’t treat “visibility” or “SEO” as a collection of separate tactics. Their data is accurate everywhere AI looks. Their reviews reflect real, recent customer experiences. Their local presence is consistent across every platform consumers turn to. And when a customer searches – whether on Google, Gemini, or ChatGPT – they find the same credible, complete picture of the brand, regardless of where they look.

That is what it takes to win visibility and customers in this landscape. And it is exactly what Yext is built to help brands do.

Methodology

Survey conducted online in 2026 among 3,848 adults globally who reported searching for local businesses. Respondents who indicated AI use for local search in the past month constitute the AI-user subgroup (n=1,628–1,634 depending on question). Data is self-reported. Findings should be treated as directional for general population extrapolation. North American demographic segmentation referenced in Finding 01 reflects a separate survey wave of 1,120 US adults; full methodology and findings available here.